PAN-Based TDS Payments Simplified: Introduction of Single Form 141 from April 2026

Introduction

The Income Tax Department has streamlined PAN-based TDS compliance by introducing a unified Form 141. This change is effective from 1st April 2026 and aims to simplify tax deduction procedures for individuals and non-business taxpayers.

Background / Legal Framework

Under the Income-tax Act, PAN-based TDS provisions apply to specific transactions where TAN is not required, such as:

- Section 194-IA – TDS on purchase of immovable property

- Section 194-IB – TDS on rent by individuals/HUF (non-audit cases)

- Section 194M – TDS on payments to contractors/professionals by individuals

- Section 194S – TDS on virtual digital assets (in certain cases)

Historically, each section required separate forms (26QB, 26QC, 26QD, 26QE), creating fragmentation in compliance.

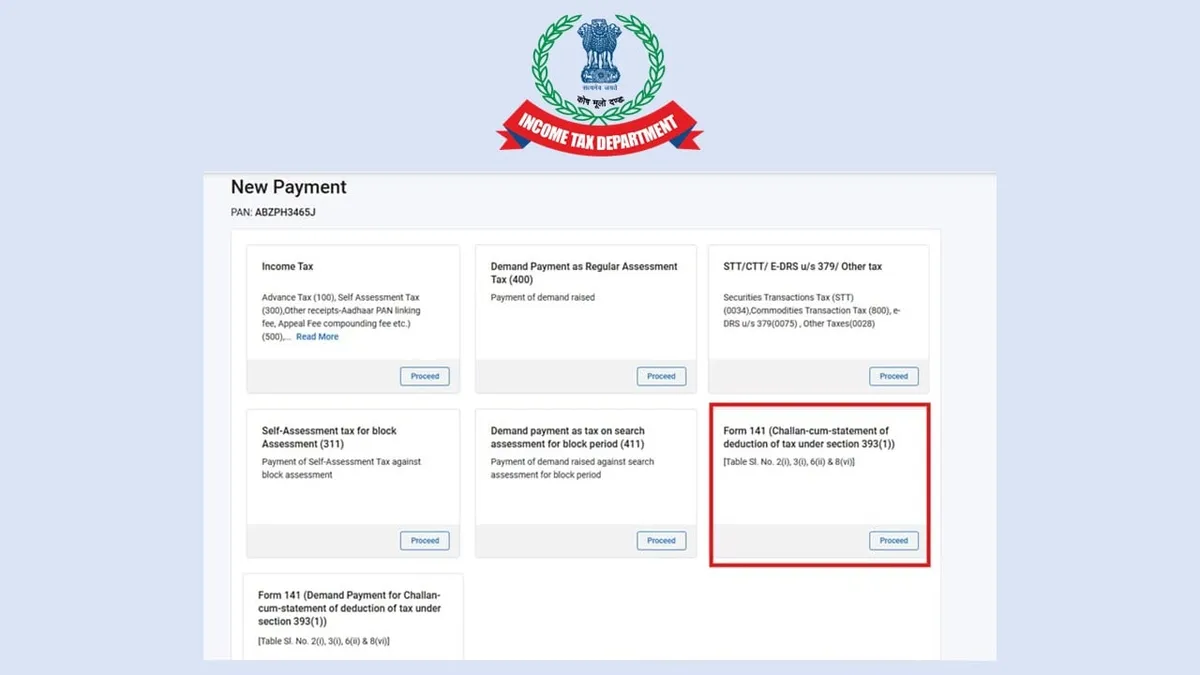

What is the Change / Update

From 1st April 2026, all such PAN-based TDS payments can be made through a single consolidated Form 141. This replaces multiple forms and standardizes the reporting mechanism.

Key Features / Highlights

- Single form for multiple PAN-based TDS transactions

- Elimination of multiple challan-cum-statements (26QB, 26QC, etc.)

- Simplified filing interface for taxpayers

- Reduced compliance errors due to uniform structure

- Likely integration with pre-filled PAN-based data

Practical Impact

- Individuals and HUFs will face significantly lower compliance complexity

- Reduced chances of selecting incorrect forms or sections

- Faster processing and reconciliation by the department

- Professionals handling bulk property/rent transactions benefit from standardization

However, initial transition issues (system glitches, mapping errors) are highly probable.

Risks / Caution / Alternative Interpretation

- Classification risk remains: taxpayers must still correctly identify the applicable section (e.g., 194-IA vs 194M)

- A single form does not eliminate liability for incorrect deduction or late payment

- Ambiguity may arise where transactions overlap (e.g., composite contracts involving rent + services)

- System dependency risk: any portal failure impacts all categories simultaneously

Action Plan

- Map all PAN-based TDS transactions currently handled (property, rent, contractors)

- Update internal SOPs to replace old forms with Form 141

- Train staff/clients on correct section classification despite unified form

- Reconcile past filings (26QB/26QC etc.) with new reporting structure

- Monitor portal updates and utilities released by the Income Tax Department

- Perform initial filings with caution during the transition phase

Conclusion

The introduction of Form 141 is a welcome rationalization of PAN-based TDS compliance. While it reduces procedural burden, accuracy in classification and timely compliance remain critical.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from Thunuguntla & Associates. Reach out to discuss your requirements.