GST Advisory on Re-Computation of Interest in Table 5.1 of GSTR-3B (Feb 2026 Glitch Impact)

Introduction

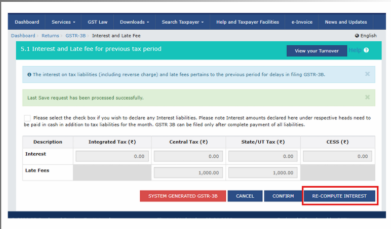

The GST Portal has enabled a facility for re-computation of interest in GSTR-3B, addressing inaccuracies arising from a system glitch observed in the February 2026 tax period. This update is critical for taxpayers who may have been subjected to excess or incorrect interest liability.

Background / Legal Framework

Interest under GST is governed by Section 50 of the CGST Act, 2017, which mandates payment of interest on delayed tax payment. The computation is system-driven in GSTR-3B, particularly reflected in Table 5.1.

However, judicial precedents and amendments (notably the proviso to Section 50(1)) clarify that interest should be levied only on the net cash liability, except in cases involving fraud or suppression.

What is the Change / Update

The GST Portal has introduced a functionality allowing taxpayers to re-compute interest in Table 5.1 of GSTR-3B where system-generated values are incorrect.

This is primarily in response to:

-

A technical glitch affecting February 2026 returns

Need help with this? Talk to Thunuguntla & Associates → -

Incorrect auto-population of interest liability in certain cases

Key Features / Highlights

-

Taxpayers can manually recompute interest instead of relying solely on system values

Need help with this? Talk to Thunuguntla & Associates → -

Applicable specifically where discrepancies are identified

-

Helps avoid excess payment of interest

-

Aligns with legal position of interest on net cash liability

Practical Impact

-

Taxpayers who blindly accept system-computed interest risk overpayment

-

Incorrect interest once paid may require refund process, leading to working capital blockage

-

Increased responsibility on professionals to validate computations before filing

Risks / Caution / Alternative Interpretation

-

The portal allowing edits does not override statutory provisions—incorrect recomputation may trigger notices

-

Department may dispute taxpayer computation if not backed by proper working

-

No automated audit trail clarity yet—future scrutiny risk remains

-

Ambiguity persists in cases involving ITC reversals and re-availment timing

Action Plan (What Taxpayer Should Do Now)

-

Review February 2026 GSTR-3B filings for any excess interest computation

-

Recompute interest independently based on net cash liability principles

-

Maintain detailed working papers supporting recomputation

-

Use the portal facility cautiously to update correct interest

-

Evaluate refund eligibility if excess interest already paid

-

Document justification to handle potential departmental queries

Conclusion

This facility is a corrective step but shifts responsibility onto taxpayers and professionals. Interest computation should now be treated as a validated figure, not a system-driven default.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from Thunuguntla & Associates. Reach out to discuss your requirements.