TDS Due Date for April 2026 — What Changes Under the New Income Tax Act, 2025

You deducted TDS in April 2026. You have time until 7th May 2026 to deposit it. That part hasn't changed.

What has changed — and this is where most people will slip up in the first quarter — is the law governing that deposit. The Income Tax Act, 1961 stood repealed on 31 March 2026. From 1 April 2026, every TDS transaction is governed by the Income Tax Act, 2025. The April 2026 deposit due on 7 May is the very first one to fall under the new framework, and filing it with old section references like 194C or 194J will make your return technically defective.

The structural change everyone needs to understand

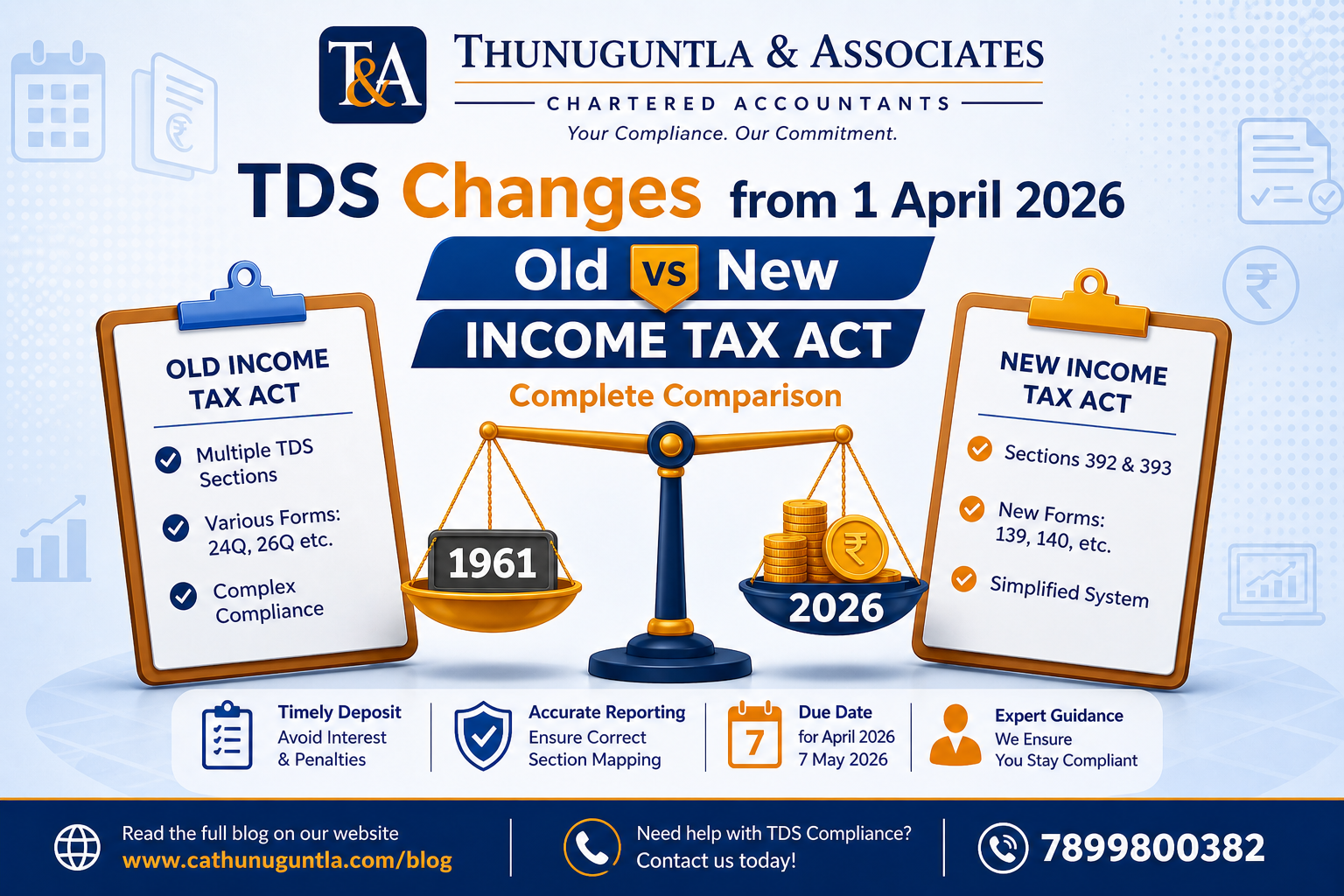

The old Act had over 60 individual TDS sections. The new Act consolidates all of this into just three parent sections — Section 392 covers salary TDS, Section 393 covers all non-salary payments to residents and non-residents, and Section 394 covers TCS. The rates and thresholds are largely unchanged; what changed is the structure, the section references, and the form numbers. Everything your team has memorised from 192 to 194T now maps into these three sections. Same tax policy, completely new numbering.

| Old Section (ITA 1961) | New Section (ITA 2025) | Payment Type |

|---|---|---|

| 192 | Section 392 | Salary |

| 194C, 194J, 194I, 194A, 194H, 194Q | Section 393 | All non-salary TDS |

| 206C series | Section 394 | TCS |

Forms have changed too

Your accounts and HR teams need to update their references immediately. Form 24Q is now Form 138. Form 16 is now Form 130. Form 16A is now Form 131. And in a welcome move, Form 15G and Form 15H have been merged into a single new Form 121. Using old form numbers for Tax Year 2026–27 transactions creates non-compliance, not just inconvenience.

The transition rule — get this right

The governing law depends on when the earlier of credit or payment occurs. If that event falls on or before 31 March 2026, the Income Tax Act, 1961 applies. If it falls on or after 1 April 2026, the Income Tax Act, 2025 applies — and the subsequent deposit date does not alter this. So a professional fee credited in March 2026 but paid in April still attracts old Act provisions. An April 2026 payment, regardless of when it gets deposited, falls under Section 393. No grey area here.

One substantive change worth flagging

Manpower supply services are now explicitly included as "work" under Section 393 — the provision corresponding to old Section 194C. The earlier ambiguity around whether deploying contract workers constituted a works contract is gone. TDS applies at 1% for resident individuals and HUFs, and 2% for all other cases, from 1 April 2026. If your business has been skipping TDS on labour deployment or contract staffing invoices based on that old ambiguity, April 2026 is the point to correct it.

Before you deposit on 7 May

Verify that your challan carries new section codes and not the old 194-series references. Confirm your software or ERP has been updated for ITA 2025 mapping. Shift vendor declarations to Form 121. And note that the terminology has changed — FY 2026–27 is now called Tax Year 2026–27 under the new Act, replacing the old Previous Year and Assessment Year framework. Systems are required to be updated to reflect new section numbering, terminology, and reporting requirements under the Income Tax Act, 2025.

The rates are the same. The law is not.

Have Questions? We're Here to Help

Get expert advice from Thunuguntla & Associates. Reach out to discuss your requirements.